الأخبار

IWD 2026: Are Women Fully Included in Africa’s Digital Financial Future?

بواسطة Sabine Mensah, Deputy CEO, AfricaNenda Foundation - 6 مارس 2026

Africa's payments landscape is undergoing rapid transformation. Instant Payment Systems (IPSs) now connect millions of users across cities and rural areas, facilitating real-time personal, business, government, and cross-border transactions. According to the 2025 State of Inclusive Instant Payment Systems report published by AfricaNenda Foundation, 36 IPSs are now live across 31 countries, processing approximately 64 billion transactions valued at nearly USD 2 trillion in 2024.

The infrastructure is scaling rapidly.

Despite the expansion of instant payment systems, benefits remain unevenly distributed particularly along gender lines. Women across Africa face unique and intersecting barriers such as limited phone ownership, lower digital literacy, constrained mobility, and restrictive socio-economic norms. These challenges can exclude women from fully participating in and benefiting from digital payment ecosystems, turning a “real-time” promise into real-world exclusion.

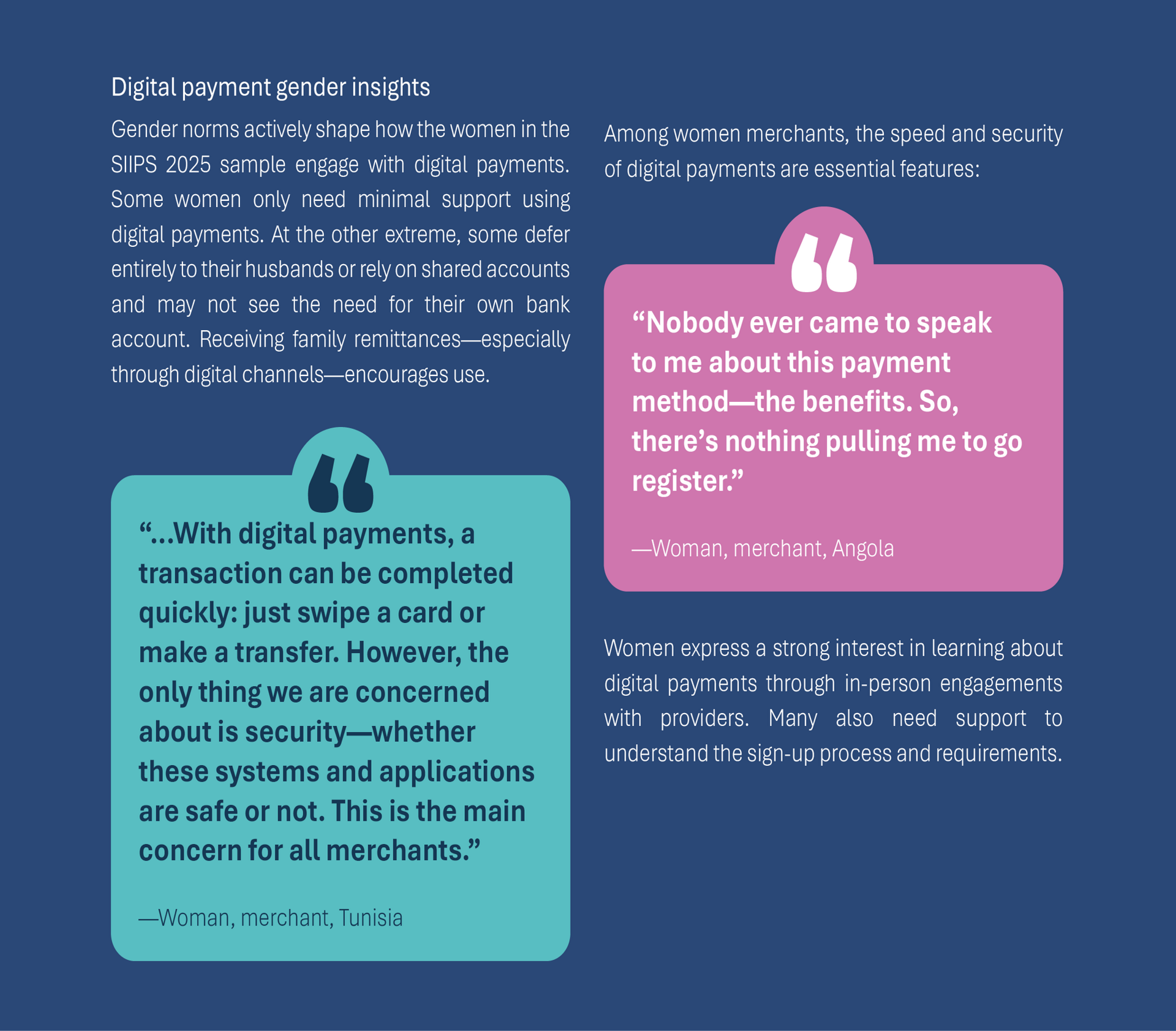

SIIPS 2025 reveals important gendered dynamics. Women are more likely than men to say they need support registering for digital payments. They are less likely to hold formal jobs and more likely to have lower incomes, reducing both opportunity and frequency of digital transaction usage.

Digital Payment Gender Insights: SIIPS Report 2025

Confidence also plays a significant role. Women tend to report lower confidence in using digital payments, often due to fears of fraud, technical errors, and difficulty resolving disputes. Many rely on word-of-mouth information rather than official provider channels, increasing exposure to misinformation. Some women share accounts with spouses or other household members instead of owning accounts independently, limiting privacy and financial autonomy.

Yet, despite these barriers, women clearly recognize the value of digital payments, particularly for receiving remittances and purchasing household goods or business supplies. The demand is present. The gap lies in design, trust, and usability.

What systemic barriers continue to limit access and meaningful usage?

Access alone is not the challenge. Many women hold transactional accounts. The issue is depth of engagement. Structural income disparities, social norms, limited recourse mechanisms, high or opaque transaction fees, and weak consumer protection frameworks all undermine sustained use. At AfricaNenda, we have learned that access alone is not enough, true inclusion comes when women can use payment systems in ways that fit their everyday realities and contexts.

Fraud or even the perception of fraud risk can significantly deter adoption. Where dispute resolution processes are unclear or inaccessible, trust erodes quickly. Without intentional safeguards, the very systems designed to expand opportunity can unintentionally reinforce existing inequalities.

What concrete actions are needed to move from commitment to measurable impact?

First, policymakers and regulators must embed gender responsiveness into IPS governance and regulatory frameworks. Proportional KYC requirements, tiered account structures, affordable pricing, and robust consumer protection and dispute resolution mechanisms are essential to building trust and lowering barriers. National strategies need gender targets and mandatory sex-disaggregated reporting to hold providers accountable.

Second, payment system operators, financial institutions, fintechs, and PSPs must design with women’s lived realities in mind. Clear communication through trusted channels, digital literacy support, privacy-enhancing features, transparent pricing, and simplified user interfaces can significantly improve confidence and sustained usage.

Third, gender-disaggregated data must guide decision-making. Without measuring differences in registration, usage, transaction types, and drop-off points, meaningful gaps remain invisible. what gets measured gets improved and gender data is part of our compass for true financial inclusion.

Instant payment systems are more than technical infrastructure; they are instruments of economic participation and empowerment. When designed inclusively, they can enable women to transact securely, grow businesses, receive income directly, and strengthen financial independence. When gender targets are written into policy and backed by data, inclusivity stops being optional and becomes systemic.

This International Women’s Day, “Rights”. Justice. Action.” challenges us to move beyond access and toward agency and empowerment. The infrastructure exists. The opportunity is clear. Now is the moment to ensure that Africa’s digital payment revolution delivers not only speed and scale, but fairness, trust, and measurable impact for all women and girls.

AfricaNenda Foundation is building a gender responsive IIPS framework which will outline what is consider neutral in infrastructure development and what can be done collectively to work toward gender intentional and transformative outcomes to drive massive access and usage of IIPS by women anywhere in Africa. Stay tuned!